- Dec 6, 2017

- 177

- 0

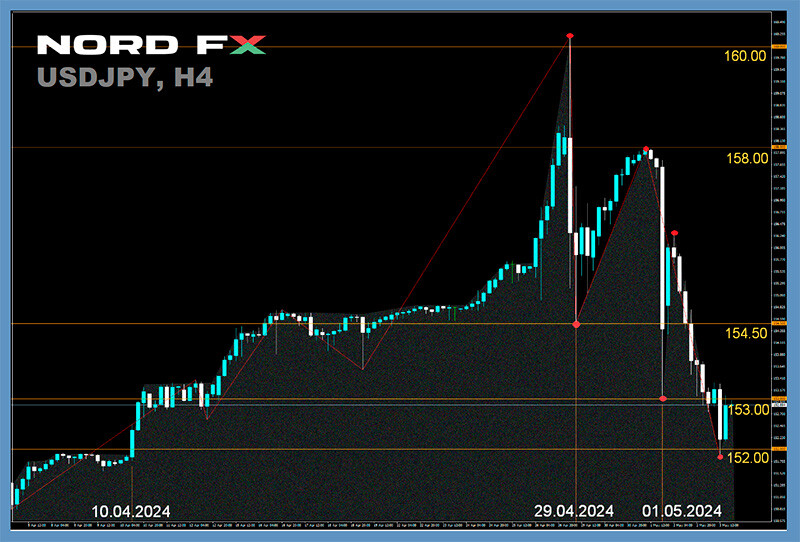

USD/JPY: A Break Above 152.00 – A Matter of Time?

For two and a half weeks, USD/JPY has been moving in a sideways channel, unsuccessfully attempting to rise above 152.00. Fear of possible currency interventions by the Japanese Ministry of Finance prevents the bulls from breaking this resistance. While actual interventions have not yet occurred, there has been plenty of verbal intervention from high-ranking Japanese officials. For example, Finance Minister Shunichi Suzuki once again stated that the authorities are closely monitoring the situation and do not exclude any options to combat excessive currency movements.

Despite such statements, the yen remains under pressure, increasing the likelihood of the pair's bullish trend continuing. According to strategists at the American bank Brown Brothers Harriman (BBH), the continuation of the upward rally is just a matter of time. They write that a very gradual tightening of the Bank of Japan's policy, coupled with a softer than previously anticipated Federal Reserve easing cycle, serves as a fundamental catalyst.

The market sentiment, according to several analysts, does not contradict BBH's forecast. Currently, according to statistics, most traders (up to 80%) are in sell positions for USD/JPY, which increases the chances of the market moving against the crowd.

The pair finished last week at 151.61. As for its near future, 80% of experts (i.e., the same percentage as the traders) sided with the bears for the pair, voting for further strengthening of the American currency, while the remaining 20% voted otherwise. Technical analysis tools are clearly unaware of fears regarding possible currency interventions. Therefore, all 100% of trend indicators and 85% of oscillators on D1 point north, with only 15% of the latter looking south. The nearest support level is located in the zone of 150.85, 149.70-150.00, 148.40, 147.30-147.60, 146.50, 145.90, 144.90-145.30, 143.40-143.75, 142.20, and 140.25-140.60. Resistances are placed at the following levels and zones – 151.85-152.00, 153.15, and 156.25.

No significant events related to the Japanese economy are scheduled for the upcoming week.

CRYPTOCURRENCIES: A Week of Unexpected Announcements

After bitcoin reached a new historical high of $73,743 on 14 March, BTC/USD sharply pulled back, losing approximately 17.5%. A local minimum was recorded at $60,778. This moment marked a record outflow of funds from exchange-traded funds, with bitcoin accounting for 96%. The departure of institutional capital from the crypto sphere overlapped with many investors and miners' desire to secure profits after updating the price record. At the peak, the realized profit exceeded $2 billion per day, with a third attributable to investors in Grayscale. Analysts at JPMorgan, in a note to investors dated 21 March, mentioned the overbought condition of the cryptocurrency and the risk of a continued correction.

However, a further downfall did not occur; the market sentiment changed. While crypto funds continued to lose assets, crypto exchanges registered an increase in the withdrawal of coins to cold wallets. Whales and sharks returned to accumulating the main cryptocurrency, expecting new BTC records in anticipation of or following the halving. If the net outflow amounted to $888 million in the week of 18-24 March, it changed to an inflow of $860 million in the week of 25-31 March. The record for coin accumulation by hodlers was 25,300 BTC per day. Bitcoin reached a high of $71,675 on 27 March.

The first half of the past week brought a new wave of sales; however, analysts at Coinshares believe that the absolute majority of investment companies and hedge funds are not interested in lowering BTC quotes, and whales will try to prevent a collapse below $60,000. The absence of new price records in those days was compensated by a series of if not sensational, then at least unexpected announcements made by crypto influencers.

For instance, CoinChapter reported that the head of Tesla and SpaceX, Elon Musk, declared meme coins Dogecoin (DOGE) the official currency of the colony to be built on Mars. "The brave colonists heading to the Red Planet will be rough and ruthless people. They won't drag gold bars with them. They will need a fast and fun currency that embodies the spirit of space travel. Dogecoin meets all these criteria," Musk said. One might expect such inspiring words to propel the token's price to cosmic heights, but this did not happen. Instead, it slightly declined. This may be related to the fact that the aforementioned information appeared on 1 April – April Fool's Day or All Fools' Day. Thus, it's possible that Musk was merely joking with his fans by assigning DOGE the status of Martian currency.

Attention was also drawn to a statement by the founder of the cryptocurrency exchange FTX, Sam Bankman-Fried (SBF), who was sentenced to 25 years in prison. Arrest did not prevent him from giving an interview to ABC News. In it, SBF stated that if he or another FTX employee had remained as CEO, the clients of the bankrupt exchange "would have long returned their money" at the current rate. Hence, the question arises: why not give Sam such an opportunity? Let him first compensate the clients for their losses and then go to jail.

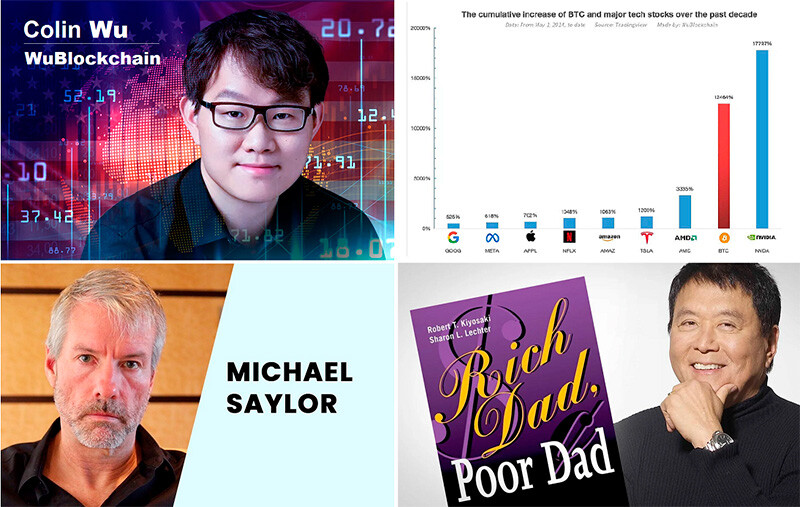

Sam Bankman-Fried is far from the only notable crypto figure of interest to US law enforcement agencies. Changpeng Zhao, co-founder and former CEO of the Binance exchange, also faced court proceedings. However, last week, he made headlines not in the criminal chronicle but in Forbes' new billionaire ranking, where he placed 50th with a net worth of $33 billion. (Bloomberg's own index attributes Zhao with assets amounting to an even larger sum – $45.1 billion). Note that the Forbes list also includes other representatives of the crypto industry. For example, Brian Armstrong, co-founder and CEO of Coinbase, was ranked 180th with $11.2 billion. In total, the publication counted 17 entrepreneurs associated with cryptocurrencies with a net worth of over a billion dollars.

Another unexpected statement came from the pen of "Rich Dad Poor Dad" author and entrepreneur Robert Kiyosaki. He is widely known for his numerous constant calls not to save "fake dollars" that will soon turn into worthless paper but to buy gold, silver, and bitcoin. Kiyosaki repeated this mantra again this time, not ruling out that bitcoin could ... crash to zero! According to him, it's possible that the first cryptocurrency is as much a fraud or a Ponzi scheme as the US dollar, euro, yen, or any other "fake" fiat currency.

As of the writing of this review on the evening of Friday, 05 April, bitcoin quotes are far from zero; the BTC/USD pair is trading around $67,680. The total market capitalization of the crypto market has slightly decreased and stands at $2.53 trillion ($2.68 trillion a week ago). The Crypto Fear & Greed Index fell from 80 to 79 points, remaining in the Extreme Greed zone.

We have already detailed the history and meaning of halvings in a previous review. Now, we remind you that the upcoming fourth halving is expected to take place soon, most likely on 20 April. After this event, according to Mark Yusko, CEO of Morgan Creek Capital, "interest in the asset will increase – many will enter FOMO mode. We should see a twofold increase in fair value. In the current cycle, it stands at ~$75,000 with downward adjustments. [...] Thus, [by the end of the year] we get $150,000," he shared his calculations on CNBC. Yusko also believes that "historically, about nine months after the event, a price peak will be formed before the next bear market."

The senior manager called the first cryptocurrency the "dominant token" and the "best form of gold". Regarding long-term prospects, the expert stated that bitcoin "can easily" increase tenfold over the next decade. Separately, the head of Morgan Creek Capital mentioned that his hedge fund likes Ethereum, Solana, and Avalanche, although they fall short of the "king-bitcoin". Mark Yusko did not mention Elon Musk's "Martian" Dogecoin at all...

NordFX Analytical Group

Notice: These materials are not investment recommendations or guidelines for working in financial markets and are intended for informational purposes only. Trading in financial markets is risky and can result in a complete loss of deposited funds.

#eurusd #gbpusd #usdjpy #btcusd #ethusd #ltcusd #xrpusd #forex #forex_example #signals #cryptocurrencies #bitcoin #stock_market

For two and a half weeks, USD/JPY has been moving in a sideways channel, unsuccessfully attempting to rise above 152.00. Fear of possible currency interventions by the Japanese Ministry of Finance prevents the bulls from breaking this resistance. While actual interventions have not yet occurred, there has been plenty of verbal intervention from high-ranking Japanese officials. For example, Finance Minister Shunichi Suzuki once again stated that the authorities are closely monitoring the situation and do not exclude any options to combat excessive currency movements.

Despite such statements, the yen remains under pressure, increasing the likelihood of the pair's bullish trend continuing. According to strategists at the American bank Brown Brothers Harriman (BBH), the continuation of the upward rally is just a matter of time. They write that a very gradual tightening of the Bank of Japan's policy, coupled with a softer than previously anticipated Federal Reserve easing cycle, serves as a fundamental catalyst.

The market sentiment, according to several analysts, does not contradict BBH's forecast. Currently, according to statistics, most traders (up to 80%) are in sell positions for USD/JPY, which increases the chances of the market moving against the crowd.

The pair finished last week at 151.61. As for its near future, 80% of experts (i.e., the same percentage as the traders) sided with the bears for the pair, voting for further strengthening of the American currency, while the remaining 20% voted otherwise. Technical analysis tools are clearly unaware of fears regarding possible currency interventions. Therefore, all 100% of trend indicators and 85% of oscillators on D1 point north, with only 15% of the latter looking south. The nearest support level is located in the zone of 150.85, 149.70-150.00, 148.40, 147.30-147.60, 146.50, 145.90, 144.90-145.30, 143.40-143.75, 142.20, and 140.25-140.60. Resistances are placed at the following levels and zones – 151.85-152.00, 153.15, and 156.25.

No significant events related to the Japanese economy are scheduled for the upcoming week.

CRYPTOCURRENCIES: A Week of Unexpected Announcements

After bitcoin reached a new historical high of $73,743 on 14 March, BTC/USD sharply pulled back, losing approximately 17.5%. A local minimum was recorded at $60,778. This moment marked a record outflow of funds from exchange-traded funds, with bitcoin accounting for 96%. The departure of institutional capital from the crypto sphere overlapped with many investors and miners' desire to secure profits after updating the price record. At the peak, the realized profit exceeded $2 billion per day, with a third attributable to investors in Grayscale. Analysts at JPMorgan, in a note to investors dated 21 March, mentioned the overbought condition of the cryptocurrency and the risk of a continued correction.

However, a further downfall did not occur; the market sentiment changed. While crypto funds continued to lose assets, crypto exchanges registered an increase in the withdrawal of coins to cold wallets. Whales and sharks returned to accumulating the main cryptocurrency, expecting new BTC records in anticipation of or following the halving. If the net outflow amounted to $888 million in the week of 18-24 March, it changed to an inflow of $860 million in the week of 25-31 March. The record for coin accumulation by hodlers was 25,300 BTC per day. Bitcoin reached a high of $71,675 on 27 March.

The first half of the past week brought a new wave of sales; however, analysts at Coinshares believe that the absolute majority of investment companies and hedge funds are not interested in lowering BTC quotes, and whales will try to prevent a collapse below $60,000. The absence of new price records in those days was compensated by a series of if not sensational, then at least unexpected announcements made by crypto influencers.

For instance, CoinChapter reported that the head of Tesla and SpaceX, Elon Musk, declared meme coins Dogecoin (DOGE) the official currency of the colony to be built on Mars. "The brave colonists heading to the Red Planet will be rough and ruthless people. They won't drag gold bars with them. They will need a fast and fun currency that embodies the spirit of space travel. Dogecoin meets all these criteria," Musk said. One might expect such inspiring words to propel the token's price to cosmic heights, but this did not happen. Instead, it slightly declined. This may be related to the fact that the aforementioned information appeared on 1 April – April Fool's Day or All Fools' Day. Thus, it's possible that Musk was merely joking with his fans by assigning DOGE the status of Martian currency.

Attention was also drawn to a statement by the founder of the cryptocurrency exchange FTX, Sam Bankman-Fried (SBF), who was sentenced to 25 years in prison. Arrest did not prevent him from giving an interview to ABC News. In it, SBF stated that if he or another FTX employee had remained as CEO, the clients of the bankrupt exchange "would have long returned their money" at the current rate. Hence, the question arises: why not give Sam such an opportunity? Let him first compensate the clients for their losses and then go to jail.

Sam Bankman-Fried is far from the only notable crypto figure of interest to US law enforcement agencies. Changpeng Zhao, co-founder and former CEO of the Binance exchange, also faced court proceedings. However, last week, he made headlines not in the criminal chronicle but in Forbes' new billionaire ranking, where he placed 50th with a net worth of $33 billion. (Bloomberg's own index attributes Zhao with assets amounting to an even larger sum – $45.1 billion). Note that the Forbes list also includes other representatives of the crypto industry. For example, Brian Armstrong, co-founder and CEO of Coinbase, was ranked 180th with $11.2 billion. In total, the publication counted 17 entrepreneurs associated with cryptocurrencies with a net worth of over a billion dollars.

Another unexpected statement came from the pen of "Rich Dad Poor Dad" author and entrepreneur Robert Kiyosaki. He is widely known for his numerous constant calls not to save "fake dollars" that will soon turn into worthless paper but to buy gold, silver, and bitcoin. Kiyosaki repeated this mantra again this time, not ruling out that bitcoin could ... crash to zero! According to him, it's possible that the first cryptocurrency is as much a fraud or a Ponzi scheme as the US dollar, euro, yen, or any other "fake" fiat currency.

As of the writing of this review on the evening of Friday, 05 April, bitcoin quotes are far from zero; the BTC/USD pair is trading around $67,680. The total market capitalization of the crypto market has slightly decreased and stands at $2.53 trillion ($2.68 trillion a week ago). The Crypto Fear & Greed Index fell from 80 to 79 points, remaining in the Extreme Greed zone.

We have already detailed the history and meaning of halvings in a previous review. Now, we remind you that the upcoming fourth halving is expected to take place soon, most likely on 20 April. After this event, according to Mark Yusko, CEO of Morgan Creek Capital, "interest in the asset will increase – many will enter FOMO mode. We should see a twofold increase in fair value. In the current cycle, it stands at ~$75,000 with downward adjustments. [...] Thus, [by the end of the year] we get $150,000," he shared his calculations on CNBC. Yusko also believes that "historically, about nine months after the event, a price peak will be formed before the next bear market."

The senior manager called the first cryptocurrency the "dominant token" and the "best form of gold". Regarding long-term prospects, the expert stated that bitcoin "can easily" increase tenfold over the next decade. Separately, the head of Morgan Creek Capital mentioned that his hedge fund likes Ethereum, Solana, and Avalanche, although they fall short of the "king-bitcoin". Mark Yusko did not mention Elon Musk's "Martian" Dogecoin at all...

NordFX Analytical Group

Notice: These materials are not investment recommendations or guidelines for working in financial markets and are intended for informational purposes only. Trading in financial markets is risky and can result in a complete loss of deposited funds.

#eurusd #gbpusd #usdjpy #btcusd #ethusd #ltcusd #xrpusd #forex #forex_example #signals #cryptocurrencies #bitcoin #stock_market